Mortgage Rates Today: Now & What’s Actually Happening

FOMO-driven mortgages. For months, headlines screamed "Rates hit 7%," but what’s really going on and why does every ripple hit closer to your front door? The current moment isn’t just a financial blip; it’s a cultural trigger.

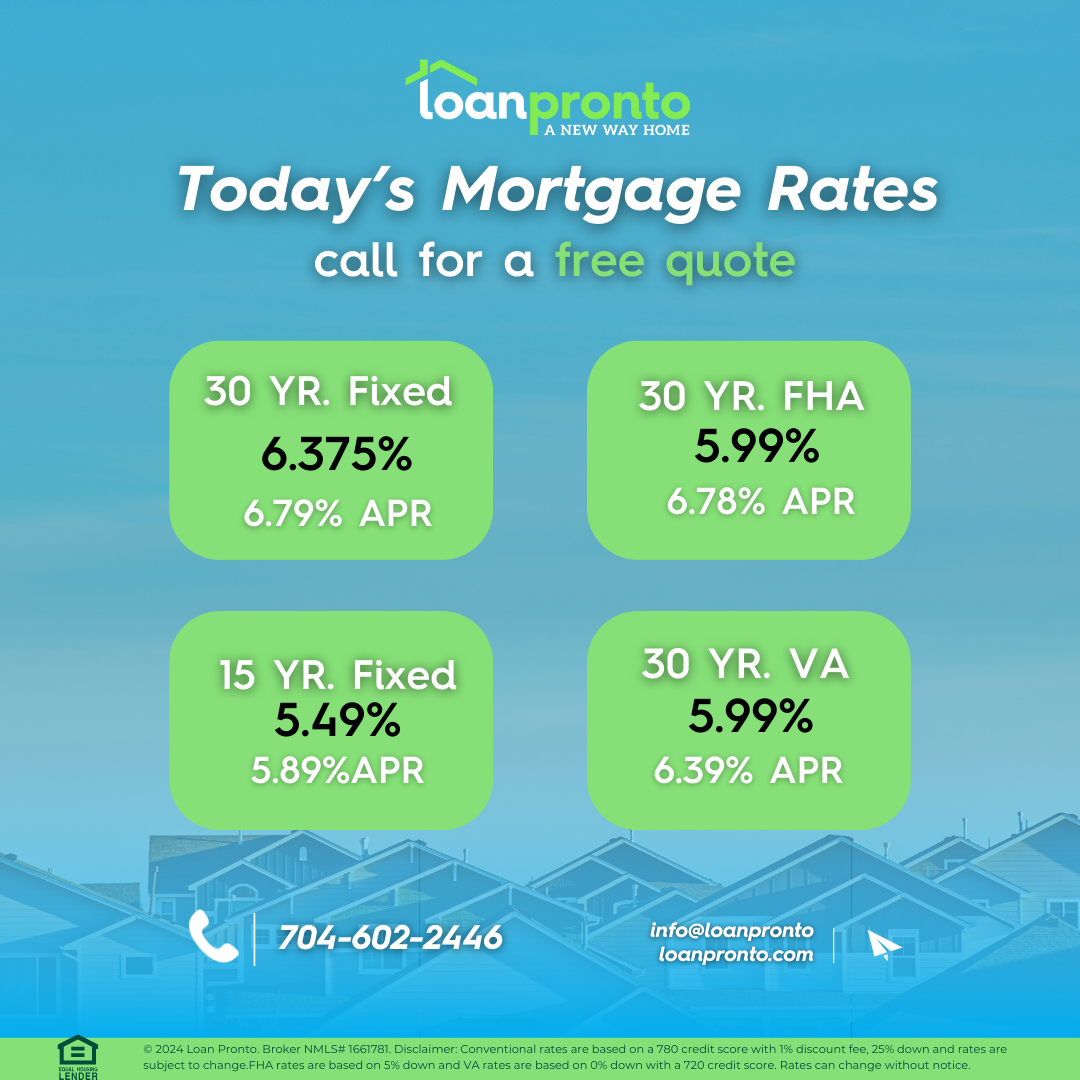

Mortgage rates today hover at a stubborn 6.9 7.4%, up sharply from 2023’s 5.8%, a jump that’s sparked online debates sharper than any policy brief. - Recent Feds rate hikes and sticky inflation have forced buyers to lock-in loans early or delay, fearing peaks but behavior’s bouncing between panic and resignation. - Data from Freddie Mac shows average 30-year mortgages sitting just above 7%, the highest since 2008.

Mortgage Rates Today: Now & What’s Actually Happening Mortgage rates aren’t just numbers they’re cultural stressors, cultural alarms, and cultural triggers. What starts as a financial signal becomes narrative fuel, shaping how millennials view homeownership, nostalgia, and trust in institutions. The crisis hits personal identity: being “house poor” feels riskier than ever, and even nostalgic internet trends around most-ideal homes now feel tinged with urgency.

Psychologically, the pause isn’t just about dollars it’s about control. When mortgage messaging screams “now or never,” it taps into a modern anxiety: miss the window, lose out to younger buyers or inherited offers, repeat past mistakes. TikTok’s “retro home hacks” trend? Not just decor it’s code for navigating finance aftershocks.

- Rate spikes feed scarcity myths: Bloggers pivot from “buy soon” to “buy fast before next move” a cycle harder to resist than logic. - Anxiety amplifies BIG decisions: Even one percentage point drives massive monthly bill differences easily $400 on a $300k loan. - Nostalgia fuels specific choices: Social media’s love for Craftsman stars and carports isn’t just aesthetic it’s comfort in a volatile market.

But here’s the blind spot: most guides treat mortgage rates like a simple spreadsheet. They don’t unpack *why* rates stay elevated despite easing inflation, or how regional floods and repair costs quietly skew local rates beyond national averages. Buyers assume a 7% rate reflects the entire nation without realizing coastal upticks or flood-prone ZIP codes spike prices locally.

And the elephant in the room: real homeownership isn’t just about rates it’s about emotional readiness. Many delayed buying not for price alone, but fear: not moving into a space tied to trauma, or buying at a “peak” they’ll regret investing in. Mental math matters, but so does mental headspace and that’s rarely >mortgage math.

So today, mortgage rates aren’t just shaping listings they’re reshaping identities, trust, and what it means to “own.” As interest complaints flood Reddit threads and LinkedIn threads, the bottom line is this: rates are high, but so is ambition and resilience. When rates feel unfair, ask: Is this market reality, or a narrative clouding judgment? Your next move might not just be financial it’s personal.

Will you lock in, wait, or question the story being told? The rates don’t care your indecision your confidence does.