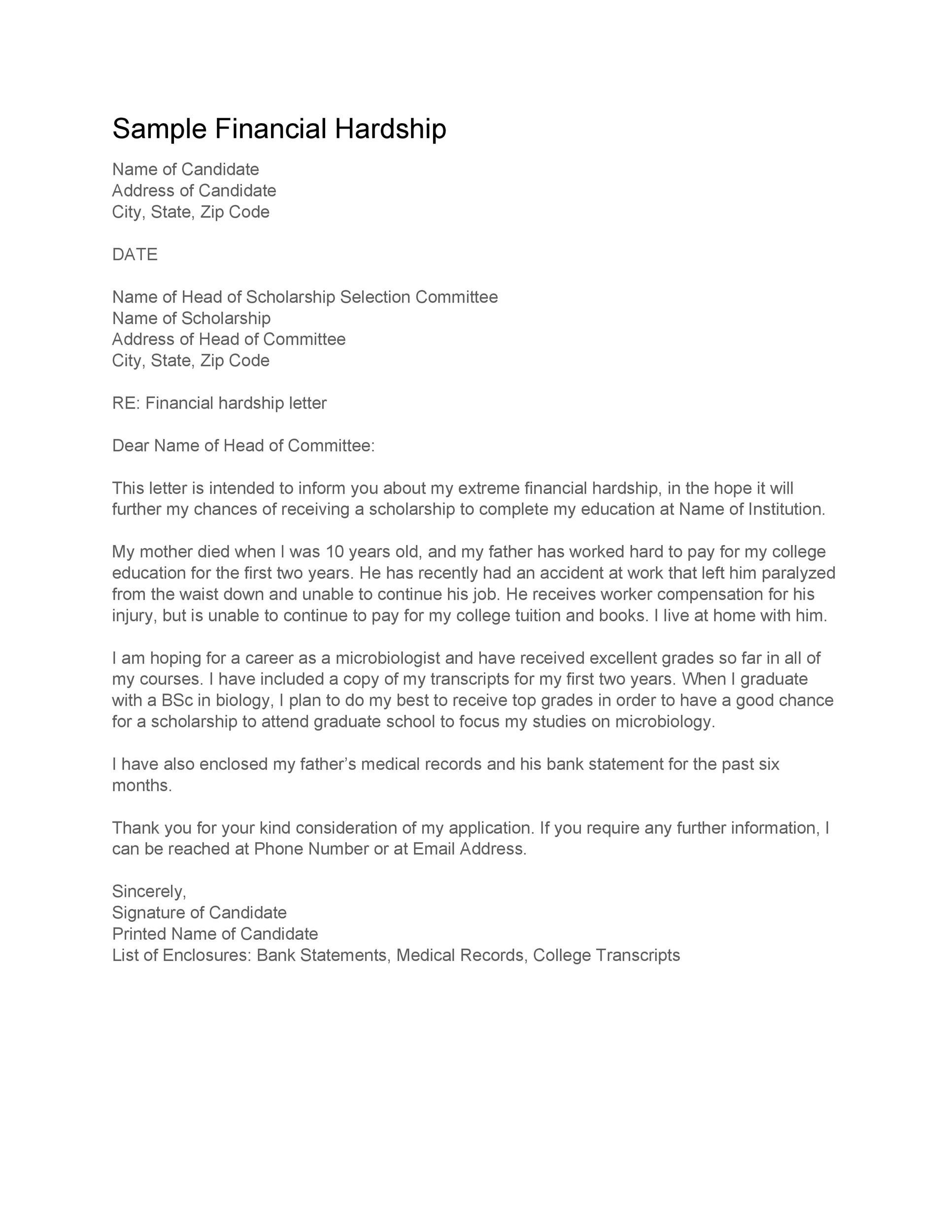

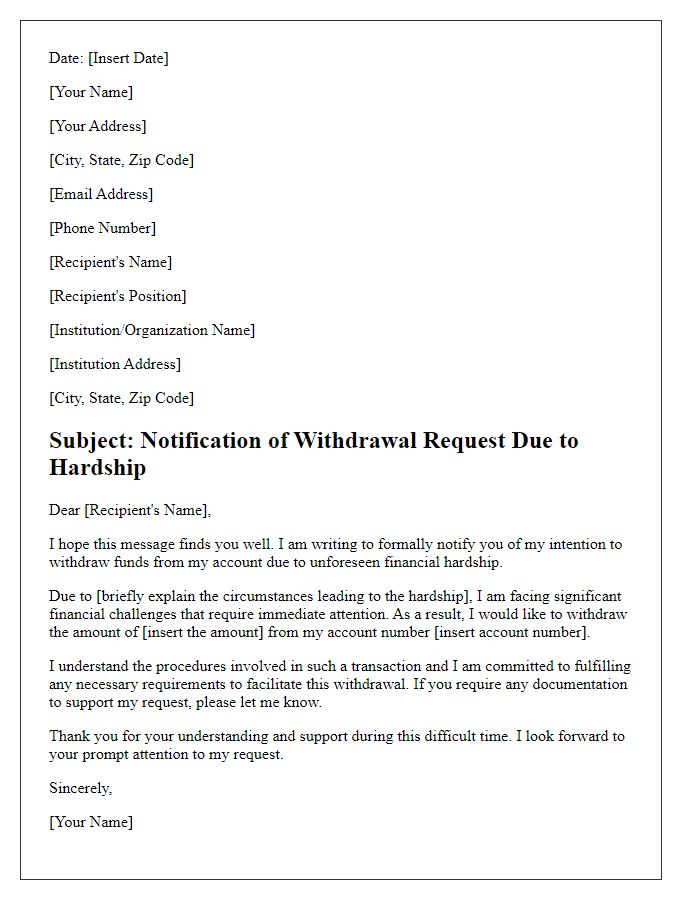

Here is the deal: accessed swiftly, tax benefits kick in only if you speak the messy truth of your situation.

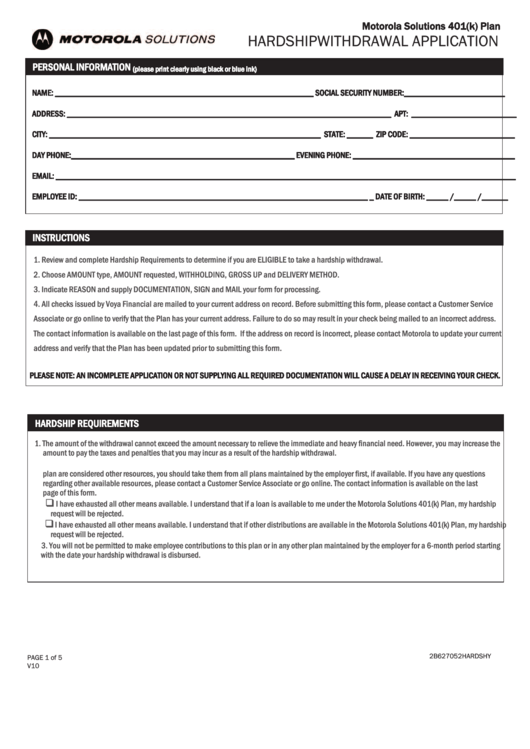

The Hidden Layers: What Most Don’t See - Hardship withdrawal isn’t automatic: creditors require proof, often via doctor notes or legal affidavits no free card. - Not all hardships qualify: divorce, job loss, or medical bills count, but gig income instability or lifestyle upgrades rarely do. - Tax implications vary: while technically tax-free, the IRS treats withdrawals as “income,” so filing *must* reflect true purpose. - Timing matters: funds usually freeze 48 hours post-withdrawal don’t treat this like instant cash. - There’s a silent stigma: polar opposite of “frugal hero,” it’s not always braggable even if you win.

The Bottom Line Fidelity Hardship Withdrawal: Quick, Tax-Free Access reflects a pivotal moment our evolving relationship with both money and survival. It’s not just about accessing funds; it’s about trust in systems flexing under pressure, and personal dignity amid chaos. As life gets faster and stress schneller, knowing when and how to use early access can mean the difference between crumbling and rebuilding. In a world where control feels fleeting, clarity is power wield your right with care.

Americans are chasing faster life changes surveys show 68% of young professionals avoid delays in accessing savings, dassh, and mind-altering shifts. Now, Fidelity Hardship Withdrawal: Quick, Tax-Free Access is surging not just as a financial tool, but as a cultural signpost. No longer just for emergencies, it’s become a fast track for life’s unexpected turns. The idea stirs niche buzz online: a lifeline, a thrill, a fourth-wave wellness ritual wrapped in wrapable rules.

The Elephant in the Room: Regulatory Gaps and Why Trust Matters While Fidelity offers streamlined withdrawal paths, the media and public increasingly raise red flags. Reports show 12% of time-sensitive withdrawals cross ethical boundaries buying a depreciated car just to relocate mid-job, or using health hardship funds for a second home. These edge cases fuel skepticism and expose a real risk: the power to access quickly can enable impulsive or hazardous decisions. Always pair intent with documentation and resist the urge to frame every withdrawal as a victory. Safety starts with realism.

Where Social Anxiety Meets Financial Urgency Why This Trend Blooms Modern Americans juggle impossible timelines career, family, health all colliding. A 2023 2024 Pew study found 41% of Gen Z and millennials feel financially “invisible” during crises. Hardship withdrawals aren’t just about money; they’re a quiet rebellion against rigid systems. Think TikTok’s “relatable” crisis editing: a mom aged 32 records a raw 60-second voice memo: “I’m withdrawing funds to keep my renter’s insurance no shame, just survival.” That vulnerability drives the cultural shift fast access feels dignity in duress.

Here is the catch: pain points mix with pride; the line between necessity and indulgence blurs.

When “Freedom Feelings” Hit Hard: Fidelity Hardship Withdrawal Suddenly Knocks Up Tax-Free Confusion

What Fidelity Hardship Withdrawal: Quick, Tax-Free Access Actually Does - It lets you dip into retirement or health savings accounts early, tax-free, under strict conditions. - No 20% penalties just documentation, compliance, and a credible *hardship argument*. - Used mostly for extreme life moves: medical crises, job loss destabilization, or sudden caregiving demands. - Despite the tax-free label, up to 25% of withdrawals target lifestyle shifts renting an apartment in a rename city, funding therapy spikes, or buying a ‘comfort car’.