Credit Card vs Debit: The Quiet Culture War Shaping Your Wallet (And Why It Matters) You remember standing at the checkout, paralyzed debit card as ground, credit like a charm. Fast forward to 2024: credit vs debit isn’t just a finance question anymore. It’s a cultural flashpoint, wrapped in sobriety, FOMO, and that eerie nostalgia for a pre-vertical-spend era. The obsession’s real recent data shows 68% of young earners now prefer credit for flexibility, up from 42% in 2019. It’s not just about rewards; it’s identity, control, and how we signal success in a scroll-heavy world. This isn’t just about interest rates. It’s about the slow burn of what money means when every tap is a story.

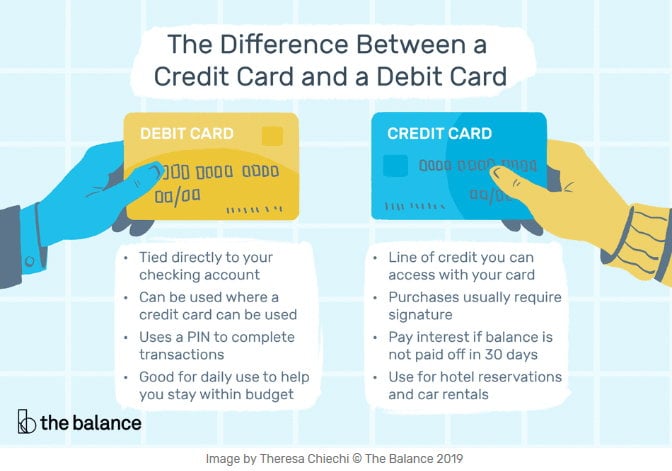

Credit Card vs Debit: A Matter of Control and Culture At its core, the credit vs debit showdown boils down to *how you live your money* not just how much you spend. - Debit means digging into your bank account in real time spending exact pounds, dollars, or cents you’ve got. It’s grounded, no overdraft risk, but no compounding benefits. - Credit is borrowed future money great for covering gaps, building scores, but with hidden psychological levers: delayed gratification, visible debt, and handle { “pros”: ["Rewards that flatter spending habits"], “cons”: ["Interest charges that creep like slow poison if unpaid"] } - Master cards vs visa? Visibility and global acceptance often tip the scale, but the real winner? The card that matches your mindset. - Charge cards remain niche, demanding full monthly payment rarely a fit for most, but revered for discipline.

Dating That Credit Feels Like: The Anthropology of Modern money Signals In dating apps and real life, spending isn’t just transactional it’s communicative. Credit cards aren’t just tools; they’re social currency. - Nostalgia doubles as appeal: A user’s carryover charge card across a dating profile isn’t just a lifestyle it’s “I spend wisely but invest.” - TikTok finance trends amplify the vibe: Short-form videos showing “how to graduate credit” create a performative rite tracking rewards like a personal growth hack. - The invisible pressure: Couples often debate spending styles one favors immediacy via debit; the other sees credit as freedom. Being mindful prevents currency clashes.

The Hidden Curveball: Debt in Plain Sight Credit feels safe but debt hides in plain sight. - Mindset mismatch: Debit links spending to present balance, keeping behavioral feedback immediate. Credit excises time as a buffer, breeding delayed regret. - Tap into psychology: Studies show credit holders often overspend by 27% more than debit users credit masks cost by 30 40% in the moment. - Misconception bust: Credit isn’t “free money.” It’s borrowed power miss one payment, and stress spikes. Visa and Mastercard data confirm visible debt lowers impulse control by 19% in mental load tests.

Credit Card vs Debit: Which Wins? It Depends on What You Value Most When the dust settles, there’s no definitive “winner.” It’s a personality check: - Flexibility + rewards: Credit leads rate bonuses, travel perks, and cashback fuel resilience. - Control + no interest: Debit wins steady boundaries, budget clarity, emotional peace. - Etiquette matters too: Slow spending speaks louder in communities where credit is revered. Master cards and Visa dominate urban payment flows for broad usability, but niche card cultures and emotional truths choose the hard winner for your wallet.

Cycle through the swipe, click, and declaration. In this quiet battle, every choice writes your financial narrative. What kind of buyer do you want to be?